Urge our legislative leaders to maintain the reforms that are reducing insurance costs and making Florida more affordable.

Key Points:

- Florida is experiencing a decrease in auto and home insurance rates, unlike most of the country.

- State leaders attribute the rate drop to 2023 legal reforms that targeted frivolous lawsuits and high legal fees for insurers.

- These reforms have reportedly encouraged more insurance companies to enter the Florida market, increasing competition.

- The author suggests further actions, such as addressing fraudulent claims and large legal judgments, to continue strengthening the market.

After the Covid crisis, Florida emerged as one of the economic powerhouses of the country. Traditionally only thought of as a destination for tourists and retirees, Florida has benefitted from the relocations of some of the nation’s wealthiest billionaires and corporate leaders, attracted not just to our climate but also to our state’s favorable tax and regulatory policies.

Only one issue has been a sticking point for everyone from working families to the most corporate elite: high insurance prices. Florida will always have cyclical fluctuations in our insurance rates due to our exposure to the hurricane corridor, but currently, we are one of the only states in the country with declining auto and home insurance rates. Why?

The Florida Chamber of Commerce and many business leaders I know point to the lawsuit reforms of 2023. Governor Ron DeSantis, former Senate President Kathleen Passidomo, and former Speaker of the House Paul Renner agreed that for too long, the billboard attorneys had been using statutory loopholes to make money from even the most frivolous lawsuits.

It was relatively easy to do because insurers were being made to pay for the legal fees of those suing them. Thus, the legal fees were gigantic for every case even when settlements were comparatively small. The impact of the one-way attorney fees was enormous, causing Florida to land on the Judicial Hellholes list. Every insurance customer in the state was paying higher premiums to account for the costs associated with the ballooning number of lawsuits. Many insurance carriers left the state completely, leaving many customers to Citizens Property Insurance, the state-subsidized insurer of last resort.

After the legal reforms of 2023, insurance rates did not go down immediately, but here at the beginning of the 2026 legislative session, rates are dropping, largely because the uncertainty of litigation is diminished, giving more companies reason to seek business in Florida again. This competition has been good for consumers as new companies are providing more products at lower prices.

I have witnessed this firsthand as a member of the board of my condo association. For the first time in many years, we have had more than one insurance provider willing to bid to insure our property. This has resulted in a huge drop in our premiums and the first drop in our association fees in nearly a decade. Yes, competition is good for everyone.

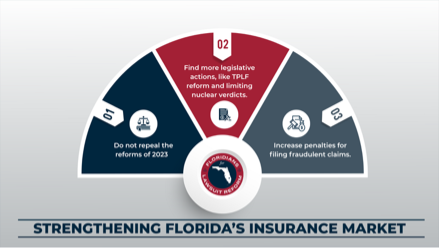

There are still some things we can do to strengthen Florida’s insurance market. First, we absolutely should not repeal the reforms of 2023. Second, we should look at some additional legislative actions including reforming third party financing of lawsuits and doing something to limit nuclear verdicts. We must also increase penalties for filing fraudulent claims. Southeast Florida and Miami specifically have long been the nation’s capital for insurance fraud. That impacts the entire market especially for those of us here on the west coast.

Let’s wish our legislative leaders well in the upcoming legislative session and urge them to maintain the reforms that are reducing insurance costs and making Florida more affordable.